GlobalData Analysis

COVID-19: A multi-channel experience is paramount for retention

The wealth management industry is undergoing a noteworthy digital transformation, but it is a two-sided coin. As the COVID-19 pandemic accelerates the importance of utilising technology for traditional players, it has also shown that a hybrid model is a must-have for digital entrants. GlobalData Financial Services writes

Y

es, the wealth space is embracing technology at a faster rate than in the pre-COVID-19 era, but learnings from robo-advice show that human advice remains necessary.

When financial markets are volatile, investors demand more communication with a human adviser for reassurance, revaluation of their investment strategy, and experienced advice.

So as robo-advice goes through its first big test of weathering a market storm, investors will prefer a human to discuss their portfolio with. The coronavirus crash will therefore cement the need for having a human option on a robo-advice platform. Current robo-advisers or new entrants who do not offer this feature should be prepared to risk losing out to hybrid competitors after COVID-19.

On the other hand, for traditional wealth managers, the COVID-19 pandemic will have forced advisers to work from home and engage with their clients through video chats, chat apps, and email or phone calls – mediums that were rarely used outside of the private wealth management tiers prior to the restrictive circumstance the world is in.

Providers should keep note that different generations will have different proficiencies in using technology, so customising this to be easily digestible for the customer will be key.

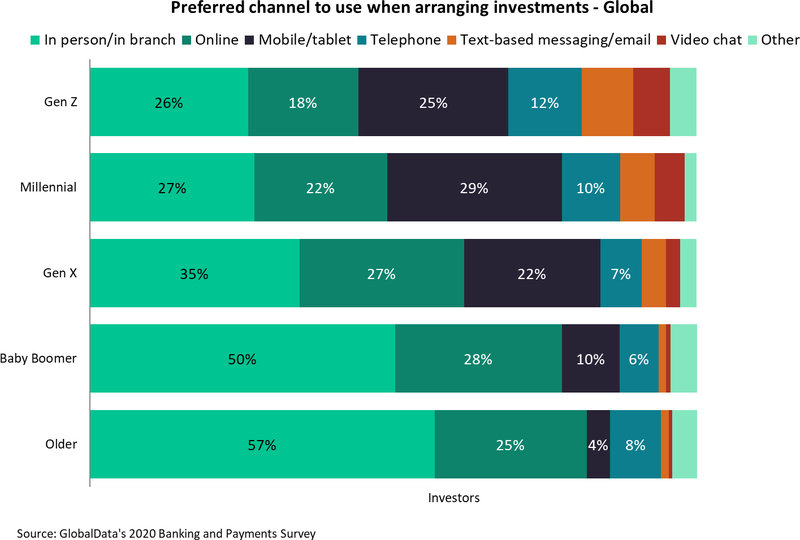

However, it will now likely become the norm as retail investors get accustomed to new ways of interacting with their adviser. Our2020 Banking and Payments Survey aptly demonstrates that clients of all generations are demanding a multi-channel experience too. Therefore, it will be vital that traditional players build on the new experience they’ve been forced to provide their customers with.

Unsurprisingly, 51% of millennials now prefer using online or mobile channels when arranging their investments. But it should also be noted that the older generation, too, embrace digital channels. Providers should keep note that different generations will have different proficiencies in using technology, so customising this to be easily digestible for the customer will be key. This will also aid in differentiating between competition as in future years, customers will be opting for players based on how good their multi-channel experience is for them, as opposed to whether they have one or not.

An individualised experience is being yearned for across financial services. Providing a multi-channel experience is one avenue to reaching the personalisation clients desire. Investors want their wealth to be managed around their day-to-day lives, and providing a wide range of options to manage their portfolio will be key. Those players who do not adapt to this demand will risk losing out to competitors who can provide a high-tech, high-touch service.

Wells Fargo offshore exit offers substantial potential AuM

Wells Fargo announced early in January that it was exiting the offshore wealth management market to focus on US resident clients. While the US retail banking giant has only a tiny fraction of its client assets under management (AuM) derived from offshore business, it would be a major boost for any bank looking to grow in the offshore wealth market, particularly for those with interest in Latin America.

The major US bank’s private wealth management arm has been ailing in recent years, with negative net new money in 2018 and 2019 along with a rising cost-to-revenue ratio. It is not surprising that the bank was looking at ways to trim costs, and the offshore wealth management sector does carry with it added regulatory burden and risk. Moreover, the scandal-scarred bank would undoubtedly be keen to avoid any further reputation risk from a relatively high-risk line of business like offshore wealth management. The bank’s account fraud scandal at its Community Bank (retail banking arm) has contributed to its poor net new money figures.

Indeed, offshore wealth management has only really been a sideline for Wells Fargo. Only 330 of its 13,512 wealth advisers were designated international advisers in 2019. This doesn’t mean its offshore business is inconsequential, however. Those 330 international advisers could account for up to $5.86bn in AuM, based on the company-wide averages. Already, many US wealth boutiques are expressing interest in hiring stranded advisers.

However, Wells Fargo could also tempt other major international private wealth managers looking to tap into the expected growth in offshore wealth management due to the COVID-19 pandemic. Half of private wealth managers surveyed by GlobalData in Q2 2020 predicted an increase in offshoring by their clients. With Latin America hard hit by the pandemic, it is likely to be at the forefront of this trend, and a large portion of the Wells Fargo offshore client base is drawn from the region.

Other major US wealth brands like Citi (already a major bank in Mexico) are most likely to benefit as advisers and their clients seek to stick with trusted banking brands. If so, there will be little noticeable shift in AuM, as these players are already giants in the US.

However, small US arms of Spanish and Canadian banks or even HSBC (also a major bank in Mexico), that have long developed a presence in the region and the US wealth market, may find Wells advisers knocking on their door too. Attracting a substantial number of Wells international advisers would have a noticeable boost to client AuM being managed by these international banks in the US. Time to refresh onboarding procedures, though hiring during a pandemic will be a challenge.