Macroeconomic Briefing

Powered by

- ECONOMIC IMPACT -

Last Updated March 2022

The US: The US economy witnessed the bouncing back of inflationary trends during the first quarter of the year 2023, after giving cues of easing inflation in Q4 2022. The nation recorded 0.4% month-on-month (MoM) growth in inflation in February 2023, which in turns points to a high inflation of 6.0% year-on-year (YoY). Owing to the decline in fuel and oil prices, the overall energy-index based inflation toned down by 0.6% MoM during February 2023.

However, the benefit is negated by rising prices amongst the necessities including food, shelter, and clothing categories. During this period, the expenses associated with food prices grew 0.4% MoM, while shelter prices rose 0.8% MoM.

As the country is coming out of its harsh winter season and as the Q1 2023 is about to conclude, businesses are fast restructuring and picking up their pace towards new or revised annual targets. In turn, the demand for new cars as well as transportation services are also on the rise, thus resulting in 0.2% and 1.1% MoM growth respectively, during February 2023. The inflation scenario in the country is expected to remain elevated in the presence of low-priced oil and petroleum commodities, a strong dollar and improving overall labor market conditions.

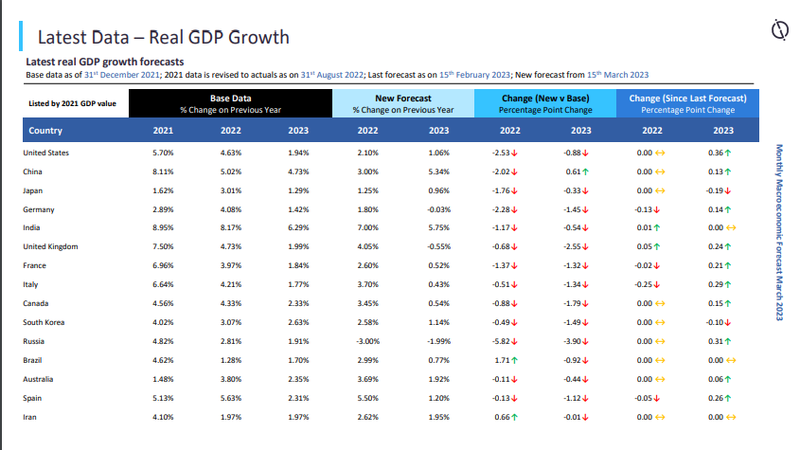

During the current monthly revision exercise, the inflation growth for 2023 is forecast at 3.94%, witnessing an upward revision of 0.44 percentage points from that of the previous forecast. Owing to the overall positive macroeconomic developments, the real GDP growth for 2023 is forecast at 1.06%.

China: The economic activities in the country retreats to moderate pace of growth with the domestic household demand slowing down, post the celebrations associated with lunar new year. The external demand for Chinese manufacturing goods is also softening, as the major trade partners struggle to tame down their own domestic inflationary pressures.

Remarkably, China is however witnessing low inflationary pressures, as the economy reported a year-on-year (YoY) inflation of 1.0% during February 2023, and against the backdrop of 2.1% YoY increase in consumer prices during January 2023. A combination of cautious consumer spending, ample availability of food products from the bumper autumn harvest of 2022, and the low prices of pork contributed to the overall decline in consumer prices in February.

The People's Bank of China (PBoC) is aiming for a healthy inflation target of 3.0% for 2023 for China, leaving behind ample scope for monetary policy relaxation and fiscal stimulus. Yet, there are no signs towards major interventions neither from the central bank nor from the government, as the economic growth is anticipated to gain momentum by its own as families and large companies eventually make use of the cash reserves they have amassed during the period of COVID-19 lockdown.

The overall inflation is also expected to move upwards to a healthier range, with the demand for oil and energy commodities expected to pick up considerably from Q2 2023, and especially during the summer. With the conservative economic growth policies and price targets, the country is expected to witness an economic growth of 5.34% for 2023.

Japan: Soaring prices strain the Japanese economic growth as the consumer price index for all commodities rose by 4.3% YoY and 0.5% MoM in January 2023, from 4.0% YoY and 0.2% MoM in December 2022.

Rising cost of commodity imports is a major factor behind these rising prices. During January 2023, the food prices grew by 7.3% YoY, within which the prices of fresh fish and seafood witnessed a massive increment of 17.2% YoY. The prices for electricity and gas also remained a concern as these sectors witnessed 20.2% and 24.3% YoY growth in prices during January 2023.

Even though there are mounting concerns over the nation staying above the inflation target of 2% for the 10th consecutive month, a change in fiscal and monetary policies is less expected in the next three months as the private household consumption continues to remain significant.

Furthermore, there is optimism amongst the various key policy makers at the government and central bank that the inflationary trends would soon touch the peak under the existing policy regimes itself. In fact, the consumer price inflation in Tokyo declined to 3.4% YoY in February 2023, from 4.4% YoY in January 2023, making it the sharpest annual decline in a month since April 2015. Though further decline in the inflationary pressure over Q2 2023 and forthcoming quarters are expected, it would be a slow and gradual process to reach the target rates under the current ultra-easy monetary policy regime. During the current monthly revision exercise, the real GDP growth for 2023 is forecast at 0.96%.

Russia: As reported by the Central Bank of Russia, the annual rate of inflation witnessed a slowdown to 10.99% in February 2023 as compared to 11.77% in January 2023. The data released by the Federal State Statistics Service (Rosstat) showed an MoM rise in consumer price index to 0.46% in February 2023. The core-CPI, excluding food and energy prices, observed an MoM and YoY growth of 0.13% and 12.69%, respectively, in February 2023.

The food prices increased MoM by 0.87%, majorly contributed by a rise in prices of fruits and vegetables by 6.69% in February 2023. The prices of motor gasoline increased in thirteen and decreased in seven constituent entities of Russia during March7 – 13, 2023. The Republic of Mari El reported the major increase in gasoline prices by 0.7% and the Chukotka Autonomous Okrug reported a major decline by 2.9%. During the current monthly revision exercise, the real GDP growth for 2023 is forecast at -1.99%

-4.4%

IMF has revised its 2020 global GDP forecast to -4.4% from an estimate of -4.9% made in June.

5.3%

The global economy is estimated to contract by 4.2% in 2020 and bounce back by 5.3% in 2021.

- Executive Summary: Embedded finance -

Last Updated March 2022

Clinical trial market impact

1,032

Trial disruption is leveling off and disrupted trials saw a small dip, with 1,032 trials still disrupted and 579 pharma/biotech companies and contract research organisations associated with disrupted clinical trials.

3,414

There are currently 3,414 clinical trials underway for Covid-19, including 172 multinational trialsroboto slab and 2,818 single-country trials.

Embedded finance hides all the legacy and complexity of banking products, surfacing only the most relevant elements, in context and at the precise moment of need. In this sense, it is the ultimate expression of customer centricity.

For banks, this is on the one hand a clear opportunity, a way to disaggregate otherwise fixed costs in infrastructure and generate fee income, while protecting themselves from disintermediation by those ahead of them in the value chain. But it also represents a risk, as banks cede part control of the direct-to-consumer relationship, and risk becoming a dumb ‘pipe’ or ‘product’ provider.

The level of disaggregation created by embedded finance will bring heightened levels of disruption, as ever-smaller pieces of banking can be unbundled and re-bundled in new ways. Many of the underlying processes, products, providers, and business models, unless delivering compelling value in this new eco-system model and reducing friction, will become redundant. Boundaries will blur so much between product, provider, and process that many business models, particularly those that do not adapt today, will be rendered obsolete.