Thought leadership

Thought leadership

Using machine learning to transform bond portfolio allocation

Ultra-low interest rates, quantitative easing, and loose monetary policy – a collective global financial comfort blanket that has been soothing us for the best part of a decade. Well, nothing lasts forever, and as we see a change in the stance of major developed-world central banks and the expected tapering of their bond-buying operations, we inevitably begin to question what will happen to the patterns of performance and correlations between bond sectors.

So what happens now?

In an environment where monetary policy tightening, it usually pays to shorten duration, reducing the sensitivity of fixed income portfolios to changes in interest rates that are felt most keenly by longer-dated instruments.

Of course, it is equally important for investors to know what level of risk they are willing to tolerate and to consider their aversion to losses, as falling bond markets are likely as interest rates rise. As we speak, bond markets, like equities, appear stretched in terms of valuation, having endured a multi-year bull market.

With the long bull market in bonds at risk, investors and their advisers should be proactive in at least considering their options. Is there something that can help them model a portfolio fit to prosper in the changing environment?

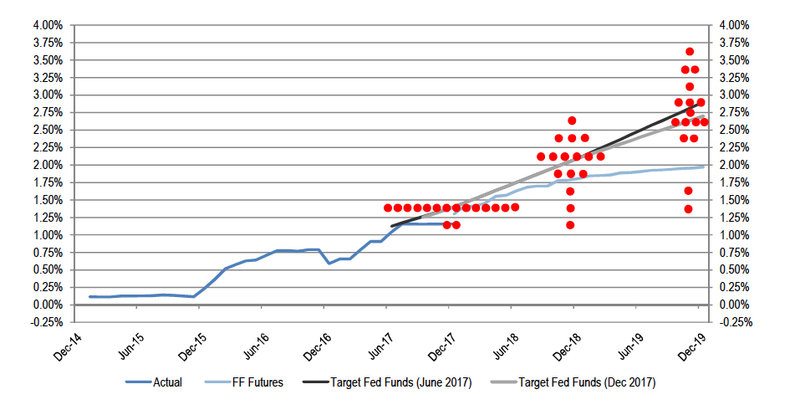

Federal Funds Rate Options Implied Forecast & Federal Reserve’s Target Fed Funds Rate Forecast per Dot Plot

Source: Bloomberg, Federal Reserve and J.P. Morgan. Note: Fed Funds options implied forecast as of 12/13/2017. Fed dot plot as of 12/13/2017 FOMC Statement.

Opportunity set (and match) in fixed income

From a global perspective, the six months to end June 2017 saw net new inflows to bond funds of US$440.6 billion compared with equities, which attracted US$207.2 billion.[1] These numbers underline the fact that many investors continue to see bonds as a fundamental element of a balanced portfolio, providing some ballast to their more volatile and risky equity cousins.

Partly for this reason, investors or their advisers may be tempted to see fixed income as a homogeneous group. While there is undoubted correlation running through the different sectors of the fixed income market, the reality is that it is comprised of separate parts that react and perform in distinctive ways – indeed they should be expected to play different roles within a portfolio. What relatively stable government bonds bring to the game is very different to that of an emerging market or high yield bond allocation, which can be expected to provide more alpha but be a more unpredictable ride.

This is a conundrum. It is easy enough to make allocations to different sectors within the bond universe; where investors and their advisers are less proficient is in picking the right combination of mutual funds and ETFs to reflect changing market conditions.

The result is often a diversified but relatively dysfunctional portfolio that does not necessarily chime with the end-investors' objectives. Where specific bets might effectively cancel each other out and where risk (interest rate or credit risk) may be at more extreme levels than realised.

[1] Global Fund Market Statistics Report For June 2017 – Lipper Analysis

Don’t just react, interact

What, therefore, is the optimal combination of the varied sectors and parts of the fixed income market as interest rates rise? How does one go about constructing such a portfolio?

One of the critical difficulties for a bond investor is the fragmentation and huge amount of data facing them, as well as the plethora of instruments in the bond market. Added to that is the inefficiency and, on occasion, illiquidity of various parts of the market.

The danger is that client portfolios are doomed to become sub-optimal or, in other words, suffer from misallocation of capital or the inevitable drift that occurs in portfolios over time, whereby the objectives of the investor and the expected performance of the underlying assets gradually diverges. The simple reason for this is that markets do not stand still. What was the appropriate combination of holdings last month may not be entirely right next month, or even next week. It is cumbersome and time consuming to continually reassess and tweak holdings to realign the portfolio with one’s objectives. What to do?

Adrian Gostick, Chief Revenue Officer of BondIT

Think it through

Artificial intelligence and data science have evolved hugely over the past few years so that they can readily provide solutions across many industries, not least investment management.

Regarding speed, there are algorithmic solutions available that can efficiently do in seconds what an investor might spend many hours to achieve. The crucial element is the swift sifting and analysis of all relevant data in an all-seeing, dispassionate manner by the software. It is a practical shortcut to a customised, optimal portfolio, slicing through the noise and, all too often, opaque nature of bond markets.

Turning to objectivity, and a technology-based approach eradicates the mistakes and subjective biases of the human mind. Where an individual may have preferences, the machine has none. It constructs the portfolio based purely on impartial observations. It is through such technology that investors can take back control, avoiding the drift towards dysfunctional bond portfolios.

At BondIT, our team has developed an approach that offers bond portfolio optimisation based on an objective analysis of millions of data as well as observations of market behaviour. New data is continuously updated, so our system learns and evolves in real time, reassuring both investors and their advisors.

What’s more, we have the added benefit of detailed, real-time, user-friendly analytics, which can be hugely useful for advisers when discussing portfolios with their clients. It provides a boost to productivity and client experience.

Be prepared

Customisation is an essential element, with tailored portfolios being generated off a single platform. Such a tool allows for existing portfolios to be uploaded and adjusted in seconds and new ones created. BondIT aggregates market data and client input and applies machine learning predictive algorithms to compare bonds, selecting those with predicted best performance for inclusion in the customised portfolios.

In an investment world where positive risk-adjusted return and performance is paramount and where efficient, relatively low-cost solutions are in demand, such technology-focused solutions are not just an response to today’s challenges but also pre-empt the environment we face in the years to come. For bonds, the income may be predetermined, but the future isn’t – it makes sense to be prepared.

Contact

Adrian Gostick

Chief Revenue Officer of BondIT

EMEA & US

Headquarters Europe & Americas:

Hamenofim 2, Seaview Building B, Floor 5, Herzliya, Israel

+972 9 779 2500

APAC

Headquarters Asia Pacific:

Level 5, Core F, Cyberport 3, 100 Cyberport Road, Hong Kong S.A.R.

+852 9308 7518