Covid-19 briefing

Powered by

- ECONOMIC IMPACT -

Last Updated September 2022

United States: In US, the all-index CPI stood at 8.5% in July 2022, compared to 9.1% in June 2022. Consumer food prices increased by 10.9% during July 2021 to July 2022, the largest increase recorded since the period ending May 1979. The consumer prices for all other items excluding food and energy increased by 5.9% in July 2022, when compared with the same period of last year.

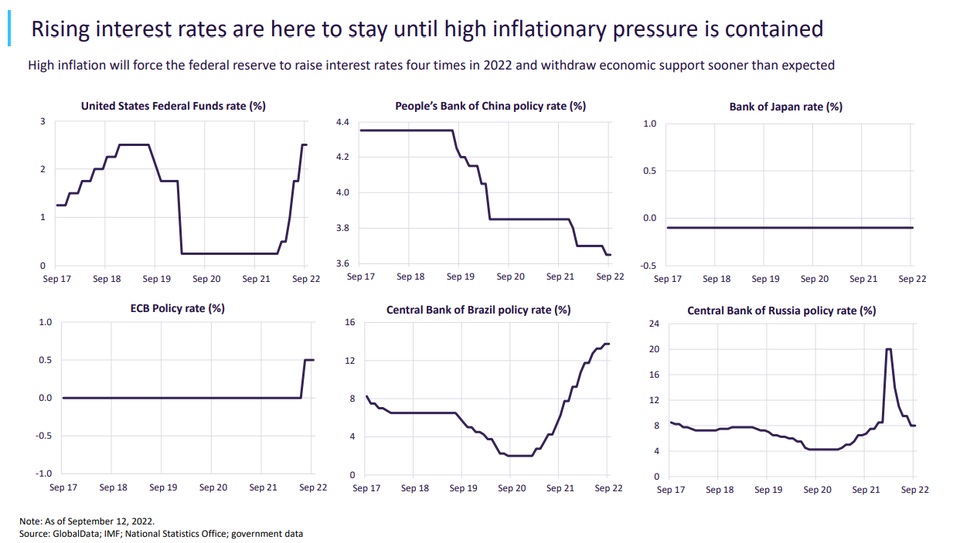

The UK: The UK’s CPI increased by 10.1% in July 2022, highest since February 1982 and a rise from 9.4% in June 2022.

The rise in inflationary pressure is attributable to the ongoing energy crisis, surging food prices, and protracted supply chain bottlenecks.

Despite risk of a recession, Bank of England to keep raising the policy rate to tame inflationary pressures.

Russia: Russia’s inflation rate declined to 14.3% in August 2022 compared to 15.1% in the previous month. However, it is now over three times as high as the central bank’s target of 4%. According to the Central Bank of Russia, inflation rate is expected to average around 14% by the end of 2022.

Germany: Inflation rate in Germany reached 7.9% in August 2022 up from 7.5% in July 2022. The inflationary pressure remains high despite the absence of the base effects caused in 2021 by the temporary reduction of VAT rates. Last six months (Dec 2021 to May 2022), the inflation rate in Germany averaged above 6%.

-4.4%

IMF has revised its 2020 global GDP forecast to -4.4% from an estimate of -4.9% made in June.

5.3%

The global economy is estimated to contract by 4.2% in 2020 and bounce back by 5.3% in 2021.

- SECTOR IMPACT: Finance -

Last Updated September 2022

Clinical trial market impact

1,032

Trial disruption is leveling off and disrupted trials saw a small dip, with 1,032 trials still disrupted and 579 pharma/biotech companies and contract research organisations associated with disrupted clinical trials.

3,414

There are currently 3,414 clinical trials underway for Covid-19, including 172 multinational trialsroboto slab and 2,818 single-country trials.

- The volume and velocity of channel shifts amid the pandemic has focused retail banks on operational agility. Redesigning core infrastructure to be more modular has helped reduce interdependencies between processes, expediting time-to-market and limiting overall complexity and cost. As the low interest rate environment continues, agile tech platforms will help banks pivot to new business models, such as Bank-as-a-Service (Baas) propositions and various types of B2B data sharing and/or enrichment. These alternative monetisation strategies will bring data security and privacy into even sharper focus, while financial wellness and ESG considerations will also become more important post-pandemic.

- Wealth managers' profits rose during pandemic-induced volatility and trading. However, the sustained high inflation of 2022 is causing a global tightening of monetary conditions and a reshaping of the investment portfolio away from the ultra-loose-rate environment that has prevailed to a greater or lesser extent since the global financial crisis.

- High inflation and supply chain disruption also means a shift in prospecting strategy, with increased priority given to sectors and markets with benefiting from higher commodities prices such as select markets of the Middle East, resource extraction regions or industries.