Covid-19 briefing

Powered by

- ECONOMIC IMPACT -

Last Updated September 2021

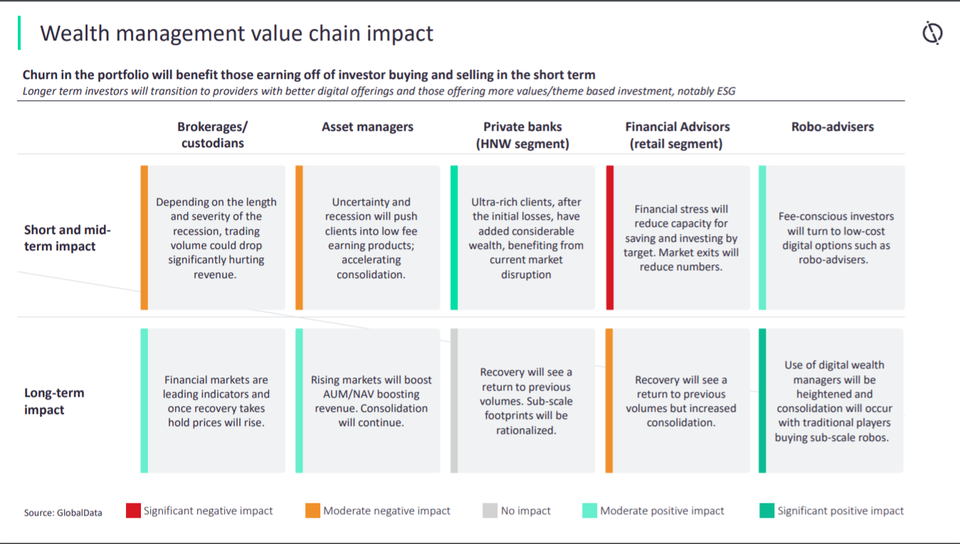

Private banks: Major international brands benefited from a flight to quality following market disruption, increasing their share of net new money. Sub-scale brands are likely to rationalize footprint, consolidation of smaller players will increase as scale becomes more important in all areas of the market regardless of geography or focus (UHNW, Swiss Private, etc).

Robo-advisers: New investors have turned to robo-advisers in greater numbers in the crisis. The US robo-advice industry is estimated to be $1tn at the end 2020, a marked increase in investor market share. The higher AUM gives major players within it the scale to be profitable and compete with even the largest traditional wealth managers, small scale robo-advisers are being acquired. Managing and retaining new investors will be a major challenge, as highlighted by Robinhood's IPO.

Financial advice firms: Independent wealth managers will need to quickly embrace digital channels and help their typically older and less technologically savvy clients adapt to the new remote era. Consolidation is expected to increase following this crisis, particularly as the need for a full suite of digital engagement tools becomes apparent in the 'new normal.'

Brokerage: Online brokerages fare well in crisis as there is ample opportunity for earning fees as investors chop and change their portfolios in light of market volatility, a prolonged recession is more of a concern. Pressure on commission rates (particularly for equity trades) will continue as investors increasingly expect near zero costs. Consolidation will continue as ever greater economies of scale are needed.

Asset managers: While volatile markets make for difficult times for investment managers, it also throws up more and new investment opportunities and can show the value of actively managed funds. The costs associated due to coping with COVID-19 will accelerate consolidation in the sector, with a number of major wealth managers buying up specialist asset managers.

-4.4%

IMF has revised its 2020 global GDP forecast to -4.4% from an estimate of -4.9% made in June.

5.3%

The global economy is estimated to contract by 4.2% in 2020 and bounce back by 5.3% in 2021.

Impact of Covid-19 on equity indices

- SECTOR IMPACT: Finance -

Last Updated September 2021

Clinical trial market impact

1,032

Trial disruption is leveling off and disrupted trials saw a small dip, with 1,032 trials still disrupted and 579 pharma/biotech companies and contract research organisations associated with disrupted clinical trials.

3,414

There are currently 3,414 clinical trials underway for Covid-19, including 172 multinational trialsroboto slab and 2,818 single-country trials.

Tracking the banking and payments sector’s Covid-19 recovery: How has the sector fared in Q2 2021?

The banking and payments sector has emerged as a relatively strong performer in the world economy when it comes to post-pandemic performance in Q2 2021.

Activity levels in the sector were 23.5% higher than they were at the end of 2019, before the pandemic decimated economies across the world. This means that, of the 18 sectors included in the analysis, the banking and payments sector ranks sixth in terms of its latest value for Covid-19 activity recovery.

The healthcare sector saw the highest sector activity levels in Q2 2021 relative to the last quarter of 2019, with the automotive, technology and apparel sectors comprising the rest of the top four.

GlobalData's sector activity metric is a derived from several of the company's research datasets. The composite index is composed using a combination of company level data on job advertisements, deals, stock prices and sentiment analysis across financial filings and news reports. It is a dynamic metric taking in millions of datapoints that can be used to track how strongly different sectors or industries are performing.

We can also delve into the component parts of the index to get a sense of exactly where companies from a given sector are over or underperforming. One of the more traditional measures of tracking performance is through the value of company stocks, which we've grouped together by industry to form a stocks performance index for each. After a dip in Spring 2020, the average sector has been performing above pre-pandemic levels since early August 2020. However, the extent of recovery varies by sector.

Banking and payments stocks generally underperformed the market in the past year, as per the chart above. By 30 June 2021, stocks in these companies - as tracked by GlobalData - were 26.2% above their starting point in October 2019.

Hiring levels are also useful in determining how confident a company is feeling about the months ahead. GlobalData's jobs index tracks job openings across thousands of companies on a daily basis, allowing us to assess that confidence in real-time and gauge which sectors are feeling Covid-19's impact the hardest.

The number of open job advertisements in banking and payments is currently at a higher level compared to most other industries, relative to their pre-pandemic norms. By 20 June 2021, the latest date for which data are available, hiring levels were 86.3% higher than those recorded prior to Covid-19's impact. This means that the banking and payments ranks second out of the 18 sectors analysed when it comes to the recovery of hiring levels.

In addition to jobs and stocks, our composite index also factors deals into account, tracking mergers, acquisitions, private equity and venture capital deals on a daily basis. This, again, can be seen as a good indicator with which to gauge how ambitious companies are feeling, with a greater number of deals indicating a more optimistic outlook.

Relative to pre-pandemic levels, the volume of financial deals in banking and payments has been higher than that of most other industries over the past 19 months.